The Single Euro Payments Area (SEPA) initiative is helping facilitate the free flow of payments and reduce the complexity of cross-border payments within Europe. SEPA zone benefits are numerous, but these payments are also creating new challenges for financial institutions and payment service providers to implement effective AML programs.

Regulated by the European Payment Council (EPC), SEPA consists of 36 European countries, including several countries which are not part of the euro area or the European Union. SEPA payments are becoming standard in the eurozone. Advantages of the SEPA zone that are driving adoption are numerous:

- Speed: Today, SEPA is facilitating fast and efficient cashless payments. SEPA Instant Credit Transfer (SCT Inst) enables parties to move money between two cross-border bank accounts in less than 10 seconds, using no intermediaries, limited to up to 15000 euros.

- Reduced costs: By simplifying cross-border payments and leveling them with domestic transfers, SCT transfers are processed at domestic rates, SEPA is either free, or costs just one euro, compared with the high-priced SWIFT wire transfers that usually cost up to $50.

- Expanded business opportunities: By facilitating cross-border payments, SEPA opens new business opportunities for companies operating within the zone contributing to the overall economic growth of the region.

Challenges of SEPA regime for financial institutions

Along with the benefits to businesses and consumers, SEPA is creating new challenges for banks and payment service providers when tackling anti-money laundering efforts.

Financial institutions participating in the SEPA regime are obligated to uphold a rigorous AML regime in line with the EU’s Fourth Anti-Money Laundering Directive (AMLD4) and the Fifth Anti-Money Laundering Directive (AMLD5). These directives require financial institutions to implement robust customer due diligence, such as verifying the identity of customers and the source of their funds. They are also required to monitor customer transactions and report any suspicious activity to relevant authorities.

With one zone and fast and easy euro transfers driving fast money transfers and higher volumes of cross-border payment traffic, correspondent banks and payment providers will be challenged to uphold these commitments.

Using legacy AML tools, the number of false positives will hover at around 98-99 %, creating a mounting challenge for transaction monitoring of SEPA transfers.

In addition, the speed of SEPA payments, with near-instant processes, will make it more difficult to detect and spot money laundering and terrorist financing activities.

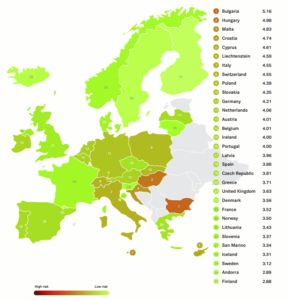

Diversity of AML regimes

Another challenge with SEPA payments is diversity of AML regimes. In the same way the eurozone faces inequality and economic gaps, the level of AML regimes over the 36 countries vary. Countries cannot be judged according to old West-East divisions when banks and payment processing providers are conducting anti-money laundering and KYC procedures.

The lowest AML risk level includes countries such as Finland, Sweden and Iceland alongside former eastern European countries Slovakia, Slovenia and Lithuania, according to the 2022 Basel AML rankings.

European Countries by AML Risk (Source: https://index.baselgovernance.org/api/uploads/221004_Basel_AML_Index_2022_72cc668efb.pdf)

At higher risk for money laundering are diverse countries with similar rankings such as Hungary, Bulgaria, Croatia, Italy, Switzerland and Cyprus,

Lack of visibility

The Single Euro Payments Area (SEPA) simplifies bank transfers of euro to member countries, in effect making cross-border payments domestic ones, as if 37 countries and territories become one. However, in reality, financial institutions handling transactions don’t have true visibility and information into the identities behind the customers and the entities they represent.

In an era of digital verification that has spawned new forms of financial crime, SEPA transfers are an

fast and efficient cross-border payments it can be easier for criminals to move money across borders and hide their tracks. Non-inclusive measures such as de-risking are not going to be an option for SEPA zone financial players especially with the fierce competition from fintechs in the region.

How AI can help solve these challenges

Global regulators have affirmed today that new AI technologies can provide a better solution to fighting financial crime compared with legacy tools.

When AI replaces human bias, transaction monitoring systems are empowered to recognize anomalies and find unknowns outside of normal behavior, including completely new typologies. Providing insights into behavior and patterns that deviate from normal activity by analyzing a multitude of risk factors enables fintechs and banks to implement a risk-based approach to effectively identify truly suspicious activity and create a full picture of customer identities, including across complex, cross-border transaction paths.

AI can effectively calculate the risks to pinpoint the suspicious activities outside of expected behavior such as the use of shell companies or sophisticated schemes that fall below the rules thresholds.

Machine learning, and especially “unsupervised” AI learns the financial behavior of each customer, builds “normal” profiles and detects unusual cases.

For the SEPA zone, this is just the kind of innovative technology approach that can solve the unique challenges of 36 countries deploying a single money transfer regime.

Written by: Yaron Hazan, VP Regulatory Affairs, ThetaRay